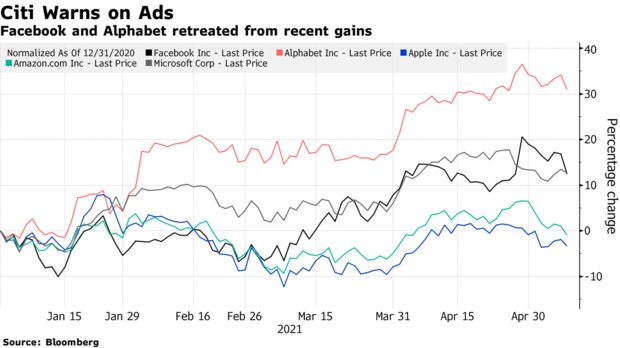

Shares of Google’s parent Alphabet Inc. and Facebook Inc. fell on Monday, leading a broad move lower in internet stocks after an American investment bank, Citi, warned about the outlook for digital advertising, a key source of revenue for the sector.

Citi downgraded both names to neutral from buy, writing that “caution is in order” for companies that derive revenue from digital advertising. While ad budgets are expected to continue shifting online, growth is likely to decelerate, and “historically, that usually isn’t bullish for multiples,” analyst Jason Bazinet wrote, according to Bloomberg.

Facebook tumbled as much as 4.3% on Monday in its biggest one-day percentage loss since January, while Alphabet was down 2.9%. The S&P 500 Communications Services index fell 1.6%.

Source: Bloomberg

Even though we see the recent decline of Facebook and Alphabet, the pair are still the best performers among the five biggest U.S. technology companies this year. Alphabet is up more than 30% so far this year, while Facebook had risen nearly 13%, as both reported first-quarter revenue that dwarfed analyst estimates when they reported two weeks ago. Microsoft rose as much as Facebook, and both Apple and Amazon.com are negative for 2021.

As the pandemic accelerated a shift toward online spending, digital ads have seen robust growth over the past two quarters. However, “the sell-side has extrapolated the recent strength for the next five years,” a view that seems too optimistic, Citi wrote. The firm expects growth will decelerate in coming quarters, posing a risk to stock multiples.

Among other names in the group, neutral ratings on both Twitter Inc. and Pinterest Inc. were reiterated by Citi, along with a sell rating on Snap Inc. The only digital-ad stock Citi recommends buying is Roku Inc., as “the connected TV market is still nascent.”

As per the firms tracked by Bloomberg, Citi is now the only one that doesn’t recommend buying Alphabet. “Forty-two firms still have a bullish view on the shares (of Alphabet). For Facebook, there are now 49 buy ratings, six holds, and three firms with a negative view on the stock.

Last week, Bloomberg Intelligence wrote that ad pricing would remain a tailwind for Facebook this year “due to demand for its ad inventory, while ad-impressions growth could taper slightly amid reopenings.” It added that despite tougher comparisons in the second half of the year, the social-media company was well-positioned to achieve 30%-plus growth in its core mobile-ad business.